- Overview

- Understanding Credit Card Surcharging in Healthcare Practices

- Implementation Options

- State-Specific Considerations

- Eligible Transactions for Surcharging

- Surcharge Rate and Limitations

- Required Signage and Disclosures

- Regulatory Responsibilities

- Refunding Transactions with Surcharges

- Billing and Reporting

Overview

Compliant Surcharging is a Bridge Payments feature that allows you to add a surcharge to credit card transactions that covers your practice’s processing fees. Compliant Surcharging is not included in all Practice Management Bridge plans. For more information about your plan, contact our Customer Care team by calling 800-337-3630 or emailing [email protected].

Understanding Credit Card Surcharging in Healthcare Practices

Credit card surcharging is the practice of adding a small fee to a patient’s credit card transaction to help offset the processing costs incurred by the practice. As credit card usage continues to rise, often carrying higher fees than debit card transactions, surcharging provides a way for practices to maintain financial health without absorbing these additional costs.

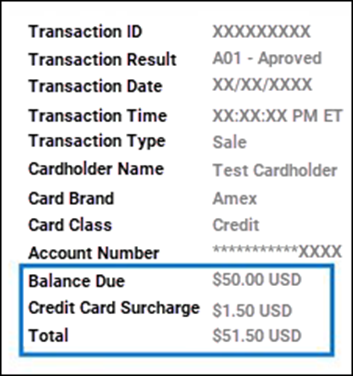

Patients will see the surcharge as a separate line item on their receipt, clearly labeled to indicate the fee. If your state mandates specific language for surcharge disclosures, you can customize the receipt label accordingly. For assistance with customization, contact your Relationship Manager or see Change the Surcharge Display Name on a Receipt.

Sample transaction receipt:

Implementation Options

Surcharging must be applied uniformly across all card readers associated with the same Merchant Identification Number (MID). You must either enable surcharging on all card readers under that MID or not implement it at all.

If your practice operates in multiple physical locations, you may choose to implement surcharging at specific locations only if each location has its own MID. Additionally, surcharging can be selectively applied based on state legality—enabled in states where it is permitted and disabled where it is prohibited.

If you implement Compliant Surcharging and have a Balance Collect site(s) to accept online payments from patients, surcharging is also enabled on the Balance Collect site(s). The same surcharging decisions you make for your physical location(s) should also be applied for your Balance Collect site(s). An individual Balance Collect site that is used for multiple locations will only have surcharging enabled on the location(s) you specified to have surcharging.

State-Specific Considerations

Credit card surcharging is not permitted in 4 states:

- Connecticut

- Maine

- Massachusetts

- California (effective July 1, 2024)

States have laws that allow surcharging but with some contingencies and dependencies on card processor.

- Colorado allows credit card surcharging up to 2%.

- New York, New Jersey, Nevada, and South Dakota prohibit surcharges from exceeding the cost that the merchant pays to accept the card.

- Texas law prohibits surcharging but allows merchants to impose convenience fees, service fees, and cash discounts (and federal courts have previously ruled against Texas surcharge laws).

- Kansas also has anti-surcharging laws that were overturned by federal courts, but merchants must include the credit card fees in the listed price to legally impose a surcharge.

- Georgia allows convenience fees on credit card transactions, but only if the merchant accepts alternative types of payments.

- Minnesota allows credit card surcharging (with some contingencies), but requires mandatory fees to be included in the advertised price of a purchase unless it can be reasonable avoided by the consumer (effective January 1, 2025).

While many states allow credit card surcharging, the specific requirement and limitations vary by state and credit card processor. Since your healthcare organization bears full responsibility for compliance, we strongly recommend obtaining expert guidance before implementing a surcharging program.

Eligible Transactions for Surcharging

When Compliant Surcharging is enabled, all credit card transactions under a specific MID will include a surcharge. The system automatically excludes debit card transactions from surcharging.

However, the following types of transactions must also not be surcharged, as required by law:

- FSA (Flexible Spending Account) cards

- HSA (Health Savings Account) cards

- Prepaid cards

- Transactions involving Medicare or Medicaid-covered services

Important Note on Medicare and Medicaid:

Practices cannot apply surcharges to patients covered by Medicare or Medicaid for services that are reimbursed by these programs. Only the official cost-sharing amounts, such as copays, coinsurance, or deductibles, may be collected. For Medicaid, these cost-sharing amounts are state-specific, and practices must ensure compliance with their state’s Medicaid guidelines.

Note on Recurring Payments:

Surcharges cannot currently be applied to recurring payment plans in Bridge Payments. This feature is planned for future release.

Note on Card on File (Vault):

The cards that you stored on file in Vault before you implemented Compliant Surcharging should not be used on the surcharging Merchant Account (location). If you want to process them on the surcharge Merchant Account (location), you will need to delete and re-create these cards stored on file in Vault.

Surcharge Rate and Limitations

All credit card transactions must be surcharged at the same fixed rate. The maximum allowable surcharge is 3% of the transaction amount. Practices cannot profit from surcharging; it is strictly to cover processing fees.

Required Signage and Disclosures

To remain compliant, practices must post surcharge notices at:

- Point of entry (e.g., front desk or entrance)

- Point of sale (e.g., card reader or checkout area)

Signage must be clear, visible, and easy to read, stating that all credit card transactions will incur a surcharge of "X" amount. For online payments via Balance Collect, a surcharge disclaimer is automatically displayed on the payment screen if the customer uses a credit card to pay. See Sample Surcharging Signage for templates.

Regulatory Responsibilities

Your practice is responsible for ensuring surcharging is implemented in a legally compliant manner, staying up to date with state-specific regulations, avoiding surcharges on prohibited payment types, and maintaining the proper signage and disclosures. Non-compliance may result in liability for the merchant.

Refunding Transactions with Surcharges

Full Refunds

The entire amount paid—including the surcharge—is refunded.

Partial Refunds

When partial refunding is enabled, users specify the amount of the original payment to refund. The system automatically calculates and includes the correct portion of the surcharge in the total refund. Partial refunding must be activated per MID. Contact your Relationship Manager to enable this feature or see Enable or Disable Partial Refunds for Surcharging.

See Issue a Partial Refund with Compliant Surcharging for instructions.

Billing and Reporting

Billing

Surcharge funds collected are automatically applied to cover your credit card merchant fees. At month-end, you’ll receive a statement from us detailing total fees applied and surcharge fees collected.

Monthly Savings

Your monthly statement includes a “Rebates” section with a line item labeled “Credit Surcharge Rebate”, showing your savings.

Reporting

Surcharge amounts will be visible in Bridge Payments in Reports > Transaction Search and your report exports. See Find the Surcharge Amount on Transactions for Reporting for more information.